Up until this year, I held the majority of my investments at Fidelity. My company 401k plan was through Fidelity, so to make things easier on myself, I held the the rest of my investment accounts at Fidelity as well.

It wasn’t until recently that I actually did the research, looked at fund performance, expense ratios, fees, etc. to see which investment firm is better, Fidelity or Vanguard.

So let the showdown begin!

My Index Fund Journey at Fidelity

In 2014, I opened an account at Fidelity after finding out about index mutual funds. An index mutual fund is basically a mutual fund that tracks an index like the S&P 500. The S&P 500 index tracks the largest 500 companies in the U.S. Research has shown that by investing your money in index mutual funds, you’ll outperform 92% of actively managed. funds.

Before 2014, I used a financial advisor at Edward Jones. But after finding out about index mutual funds, I decided to open an account at Fidelity. Plus, like I previously mentioned, my company 401k plan was already at Fidelity.

At Fideilty I was on my own. Unlike Edward Jones, I didn’t have to use a financial advisor to invest. Fidelity was appealing to me because there are no annual fees for my account and no fees for investing in Fidelity mutual funds.

I allocated my investments using a four way split between small cap, mid cap, large cap, and international index funds. I honestly don’t remember why I decided this allocation, perhaps I dreamt it up somewhere. But I used the funds FCPEX, FMEIX, FXAIX, and FSIIX.

I kept this allocation until 2018 when Fidelity debuted their no expense ratio zero funds. These were basically launched to undermine Vanguard who touts themselves as having index mutual funds with the lowest expense ratios in the game.

I got excited. Most of the financial independence retire early (FIRE) community uses Vanguard. At the time I was living in Portland, and the hipster in me liked that I was doing something different. And these new zero funds just stoked the FIRE of my inner hipster. Hold on while I go try on some skinny jeans and comb my mustache…

Okay back.

Why Vanguard is Better

At the end of 2018, I started investing in Fidelity’s zero funds. I mean, how can it get any better than NO expense ratio!?

But here’s the sneaky trick that Fidelity is playing. Fidelity is a privately owned company. The owners (shareholders) of Fidelity expect a return on their investment. This return on investment comes from the revenue that Fidelity generates from the expense ratios associated with their mutual funds. But because Fidelity’s zero funds don’t have an expense ratio, they need to get the money somewhere. Fidelity gets this money by reducing the funds dividend payout.

This was a brilliant move. Nobody is talking about dividend payouts between comparable funds, the flashy attention grabber is the expense ratio.

Now consider Vanguard, which is operated at cost. Vanguard has no shareholders to answer to. The profit that the company makes gets redirected back into its mutual funds. Based on this fact, it’s obvious that there’s no way that Fidelity can ever beat Vanguard. And here’s the proof.

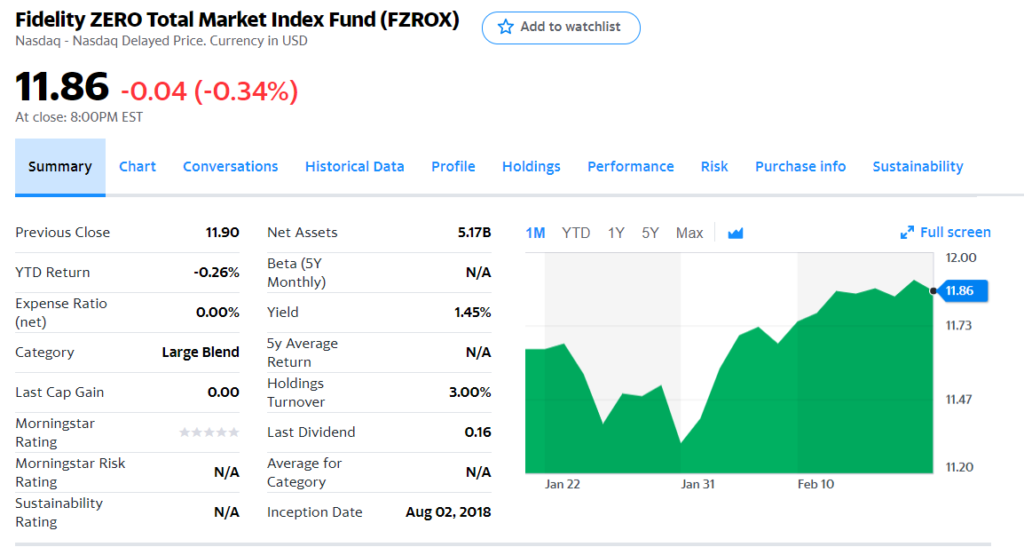

Here’s an snapshot summary of Fidelity’s ZERO Total Market Fund FZROX:

Compared to Vanguard’s total market fund VTSAX:

These two funds are tracking the same index, the total U.S. stock market. Their day to day returns should provide similar results. However, the differences are in the dividend payout. Fidelity’s FZROX had a dividend last year of 1.45%, compared to Vanguard’s VTSAX dividend of 1.77%. After subtracting out the expense ratio, that’s a difference of 0.28% in Vanguard’s favor.

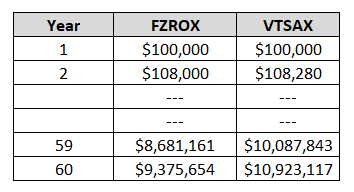

You may think, meh, 0.28% is nothing. What’s the big deal? Consider what 0.28% will look like over your investing career.

Say you have $200,000. You put $100,000 in Fidelity FZROX, and $100,000 in Vanguard VTSAX. After a lifelong career of investing, say 60 years, this is what will happen:

The big deal is if you go with Vanguard, you could potentially have an additional $1.5M in 60 years!

So, this past June I let my inner hipster die and joined the rest of the FIRE community by moving my money into Vanguard accounts. Good bye skinny jeans and mustache…

This All Sounds Great But What’s in it for You

After all this, you may think that I’m trying to sell you on Vanguard because there’s something in it for me. But I’m here to tell you, I have no affiliation with Vanguard. I’m just trying to help people from making the same mistake that I did by using Fidelity and falling for their zero expense ratio mutual funds.

Don’t be like me! I would have been so much further along my path to financial independence if I would have used Vanguard from the start.

Making the Switch to Vanguard

This past year, I transferred my accounts from Fidelity to Vanguard. It was a pretty straight forward process. I started the transfer on Vanguard’s site. For my 401k account, there was some paperwork that I had to fill out. Fidelity also put a lock on one of my accounts, so I had to call them to complete the transfer.

This past year I also started tracking my investment worth and overall net worth using Personal Capital, which I highly recommend. It’s free, convenient, and super easy to use. And as an added bonus, you get a $20 Amazon gift card just for signing up here.

Which Vanguard Fund to Invest In?

Once you get your funds transferred to Vanguard, now what? I personally invest all my money in Vanguard’s VTSAX mutual fund. VTSAX invests in every publically traded company in the United States. When you buy VTSAX you are instantly diversifying yourself with stock from over 3,000 U.S companies.

VTSAX has averaged over 14% returns the last 10 years (we’ve been in a “bull” market), and offers an additional 1.8% yearly dividend. Some people are hesitant to invest in stock mutual funds because of the day to day volatility, and I totally get it. For those that want a less volatile investment allocation, you can diversify yourself with Vanguard’s total bond market index fund (VBTLX). Depending on your risk tolerance you can allocate 10-40% of your investments to VBTLX. The more bonds you have in your portfolio, the less volatile it will be.

But for me, instead of worrying about what happens on the day to day, I keep it simple and just buy some VTSAX and forget about it. History shows that over the long run, nothing provides a better return on your investment than stocks.

And when you’ve retired early you can laugh at all your friends who kept their money at Fidelity.

Cheers to Early Retirement!